The air is going out of the customer experience software balloon

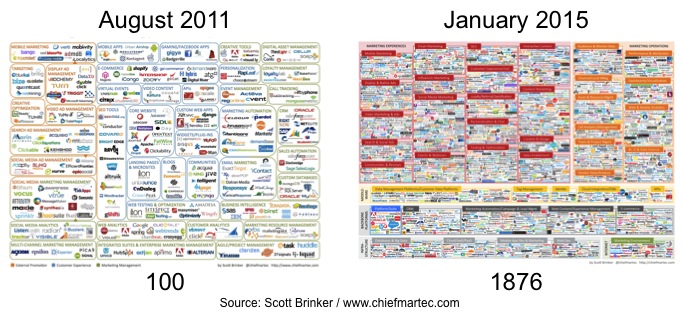

Scott Brinker’s famous marketing technology “super graphic” has charted the explosive growth of that software landscape, from about 100 vendors in 2011 to nearly 1900 in 2015.

The stunning increase in vendors and software solutions is evidence of several undeniable trends, including the digitization of marketing and the consumer expectation for improved customer experiences (CX). (At DCG, we consider martech to be part of the broader customer experience management [CEM] software ecosystem.)

Blowing up a very big balloon

But if digitization and CX are served and supported by the vendors, it is simply money that powers the growth of the software space. The best way to think of the super graphic is that it’s a balloon that increased in size by 1776% over four years, thanks to the powerful lungs of venture capitalists, angels, and other investors.

You don’t have to use that other b-word in order to recognize that the exuberance of this investment phase is a couple of letters beyond rational. Customer experience management is an inescapable imperative, but it doesn’t justify, and can’t sustain, 64 display and native advertising solutions, nor another 88 in content marketing, nor 112 (!) in social media marketing.

The fact is that very, very few of this class of 1876 are profitable. Our analysis shows that the vast majority are for sale (officially or not), as investors attempt to extract some value.

The mighty are falling

This isn’t all about startups, of course. Plenty of established companies have chased the Golden Snitch of CEM in the last few years, with varying degrees of enthusiasm, savvy, and success.

The stragglers are now limping off of the field. In mid-January, Intuit announced the sale of Demandforce, the marketing automation and communications platform it acquired for over $420 million in 2012. (You can bet it was sold at, um, a considerable discount.)

Then, on January 20, SDL’s year end trading update revealed the Board’s intention to refocus on translation, web content, and documentation technologies, while pursuing the sale of three “non-core,” CEM-related products: Campaigns, Social Intelligence, and SDL Fredhopper. (Yes, one of the most absurd product names in human history.)

Similarly, Teradata intends to shed its marketing software division, where revenue was down 9%, to $143 million, in 2015.

And, when HP split in two, it parked the legacy Interwoven TeamSite WCM product in HP Inc., with PCs and printers, rather than in HP Enterprise, with the rest of the software products. The argument is that it’s about balancing out the relatively low margin hardware with a dose of high-margin TeamSite software. Occam’s razor dictates that it’s because they want to preserve a neat, stand-alone product that’s easier to extract and sell. (Plus, a serious CEM strategy would entail integrating TeamSite more thoroughly with other software assets, such as Autonomy.)

“Peak MarTech”

Scott Brinker believes that 2016 will be the year of “peak martech,” as new entrants (also in some new categories) are outnumbered by those that exit through acquisition, consolidation, redefinition . . . or exhaustion. (And, you’ll be relieved to know he’s pledged that the 2016 graphic will have fewer vendors, whether by fact or by design.) Still, he argues that “the rate of marketing tech adoption still has tremendous growth ahead.”

But it’s worse: The “Adblockalypse”

I think he’s right, but too optimistic on both counts. First, the digital advertising space is in turmoil. The dramatic rise of ad (and tracking) blockers in 2015, the revelations (or rather, the puncturing of the mass collective self-denial) about ad fraud, and the IAB’s astonishing admission that it had systematically encouraged the violation of consumer’s interests and goals – these are multiple blows from which even advertising executives think digital advertising may never recover.

Since several hundred of the vendors in Brinker’s inventory are dedicated to ad tech, I expect to see dramatic shrinkage in the next 12 to 24 months.

But it’s even worse: The failure of “first gen” CEM

Second, the rise of marketing tech adoption will be – or at least needs to be – reconsidered and reset in light of the fact that all of this technology is not leading to improved experiences. As I discuss in my most recent published Insight Brief, “Content Management: The Hub for Systems of Engagement,” three major international studies show that customer experience is stuck in neutral, if not actually going backwards. For example, in the six months between Forrester’s Q1 and Q3 2015 CX Index surveys for 299 brands in the U.S., only 2.3% of the brands improved their ratings while nearly a third (28.5%) got worse.

As Connie Moore recently argued (in a blog post and an DCG Insight Brief), both end users and vendors need to take stock and redraw their strategic map for customer experience management. We believe that real progress depends heavily on higher level issues such as systems design, journey mapping, integrated process support, service provider partnerships, and far more flexible and intelligent technology selection habits – which is another reason to be bearish about technology adoption, and software vendor prospects, in 2016.